- FEATURE

- |

- MERGERS & ACQUISITIONS

- |

- FINANCIAL

- |

- MARKETING

- |

- RETAIL

- |

- ESG-SUSTAINABILITY

- |

- LIFESTYLE

- |

-

MORE

“Strong in jewelry, weak in watches”—a phrase that’s been repeated so often this year it’s become almost cliché. And yet, it continues to ring true. Richemont’s latest financial results offer no sign of reversal. In fact, they reinforce a persistent imbalance in the hard luxury world. That’s precisely why it’s worth reexamining: because acknowledging a repeated truth is often the starting point for change.

Richemont’s Q1 FY2026 report, covering the period through June 30, delivers a snapshot of the global hard luxury market in the first half of 2025. Group sales rose 6% year-on-year to €5.4 billion (3% at actual exchange rates). Unsurprisingly, its high jewelry division—home to Cartier and Van Cleef & Arpels—led the charge, growing 11% year-on-year and accounting for over 70% of total revenue.

By contrast, Richemont’s Specialist Watchmakers division saw sales drop 7% to €824 million, despite an improvement from the 10% decline in the previous quarter. The group attributed this softness to waning demand in China and greater Asia, and the high base effect in Japan.

While fashion and accessories brands under Richemont saw a modest 1% dip overall, Alaïa and Chloé still posted positive results.

Geographically, Richemont saw double-digit growth across Europe, the Americas, and the Middle East. But the Asia-Pacific region remained flat—held back by continued weakness in China. In Japan, where a strong yen deterred inbound shoppers, sales fell 15% despite stable local demand.

The takeaway? Jewelry is pulling the weight, while watches continue to fall short.

Data from the Federation of the Swiss Watch Industry paints a broader picture. In May 2025, Swiss watch exports declined by 9.5% year-on-year. Volume fell 13.4% to 1.17 million units. In the U.S.—the top market—exports dropped 25.3%, a sharp correction after an artificial spike the month before caused by tariff anxiety.

In China, imports fell 17.4%, and Hong Kong saw a 12.6% drop. Markets from Japan to Singapore also experienced mid-to-high single-digit declines. In short: the global appetite for high-end watches is cooling—and fast.

For over a century, watches and jewelry have defined the hard luxury category. But while jewelry thrives on its emotional symbolism and decorative value, watches lean heavily on craftsmanship, precision engineering, and controlled supply. These traits justify high pricing—but they’re not enough in today’s environment.

The return of tariff threats under a potential Trump administration has added new pressure. Brands like Rolex and Swatch Group have raised prices again—sometimes within months of the last hike. Rolex, for example, increased U.S. prices by 3% in May, just four months after its previous global adjustment. Analysts warn the hikes risk pricing out even affluent American buyers—and could trigger an industry-wide domino effect.

Interestingly, the steepest price increases have been on the highest-end models. Timepieces above $100,000 saw average price hikes of 17.5%, compared to just 4.2% for watches under $10,000. Export data also shows that watches priced between CHF 500–3,000 remain relatively stable, while pricier segments are slipping.

The message is clear: ultra-wealthy consumers can still afford luxury, but the middle tier—the dreamers, the aspirers—is slipping away. And they form the foundation of the market pyramid.

Some brands are responding. Rolex launched the Land-Dweller in April, a more accessibly priced series starting at €14,450. TAG Heuer relaunched its Formula 1 line with solar-powered models starting at $1,800. These aren’t budget watches—but they are sensible steps toward broader relevance.

Others are experimenting with partnerships. Swatch Group’s earlier collaborations—pairing Omega and Blancpain with the Swatch brand—successfully drew attention and foot traffic, even among skeptical Gen Z consumers.

More importantly, brands are finding ways to soften their appeal—whether by switching from gold to steel, simplifying complications, or leaning into narrative-rich branding. Logos, heritage, and anniversaries have taken center stage, helping brands reconnect emotionally with consumers.

The global narrative often casts China as a lost cause for luxury. Richemont echoed the usual talking points: sluggish recovery, muted travel retail, fading watch demand.

But China’s luxury fatigue may be more nuanced. Domestic player Laopu Gold, which has zero international presence, posted explosive growth: 167.5% revenue jump, 253.9% net profit increase. Its success is proof that Chinese consumers are still buying hard luxury—just not from the brands they once favored.

The shift? Consumers are redistributing their budgets, prioritizing local brands that feel fresh and aligned with modern values. Creative design, relevant pricing, and cultural resonance are all playing a role.

Watches, in particular, are being squeezed—not only by jewelry, but also by evolving lifestyle habits and social signals. Chinese consumers are questioning the functional and symbolic value of luxury watches. To win them back, brands will need more than history—they’ll need imagination.

In this climate, brands are doubling down on milestone marketing. Roger Dubuis (30th), Vacheron Constantin (270th), A. Lange & Söhne (180th), Audemars Piguet (150th), Zenith (160th), Blancpain (290th), and Breguet (250th) are all marking anniversaries in 2025. Product launches, immersive exhibitions, and heritage storytelling are everywhere—especially in China.

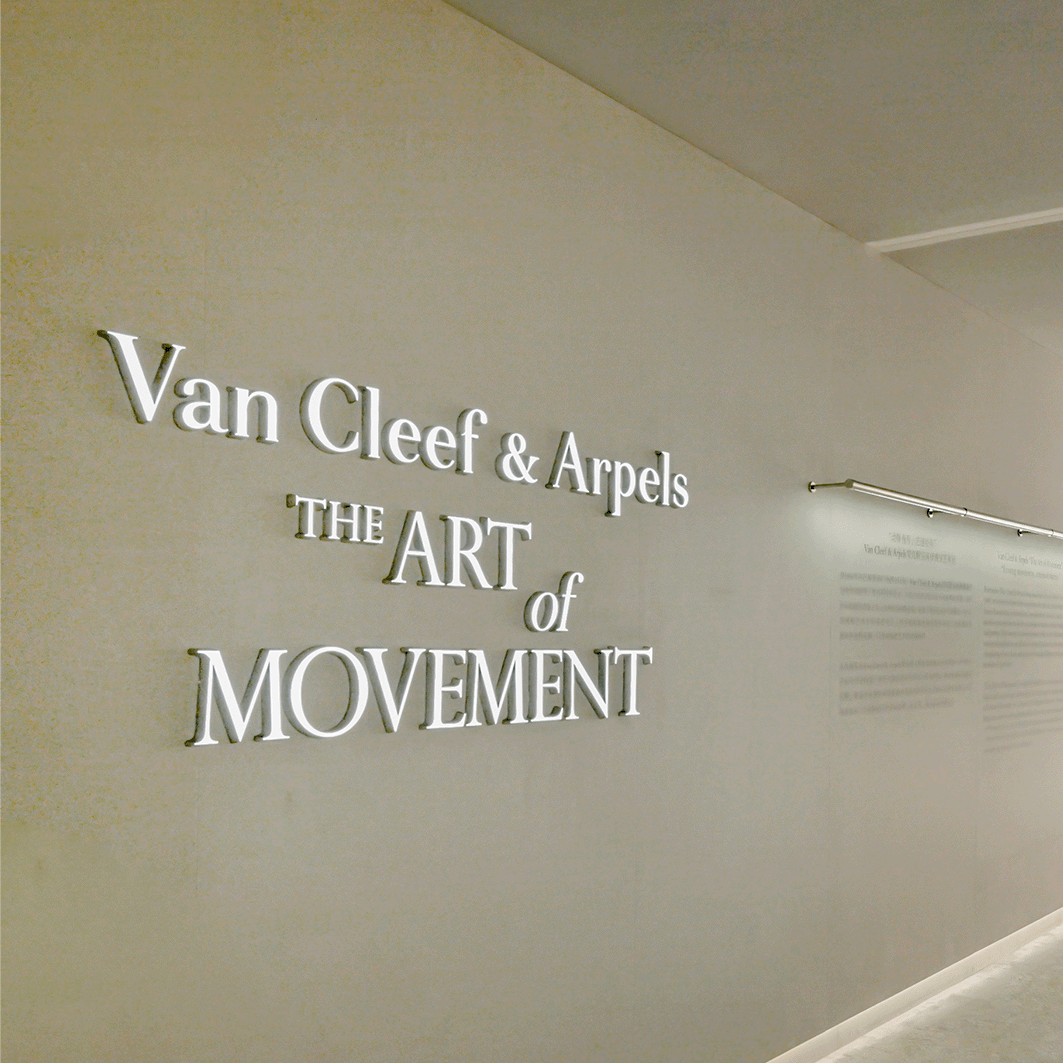

Van Cleef & Arpels, which has quietly become Richemont’s second-largest brand, even launched its first-ever watch-focused exhibition in China, signaling that the industry still sees watches as a core pillar.

But the underlying message is clear: heritage alone won’t secure future demand. As ConCall noted in its “Forecast 2025” report, the watch industry is now a buyer’s market. Brands are no longer selling scarcity—they’re selling trust, emotion, and relevance.

And in that shift lies both a challenge and an opportunity.