- FEATURE

- |

- MERGERS & ACQUISITIONS

- |

- FINANCIAL

- |

- MARKETING

- |

- RETAIL

- |

- ESG-SUSTAINABILITY

- |

- LIFESTYLE

- |

-

MORE

After a year marked by brutal market forces and internal reckonings, Kering is reengineering itself for survival—and possibly, reinvention.

By the time 2025 came to a close, Kering stood as one of the few global luxury conglomerates that had not just endured a year of contraction and investor anxiety—but had begun to recalibrate, reshuffle, and lay the groundwork for a new strategic era. The group had reached a cliff edge. And from that precarious point, it began to glow with something the industry hadn’t seen in a while: resilient energy.

While most luxury players were still surfing post-pandemic euphoria in 2023, Kering was among the first to feel the chill. Sales slid, store traffic softened, and Gucci—the group’s flagship and growth engine for much of the past decade—was visibly losing steam. By 2024, its market capitalization had plunged to levels unseen since 2021, and the myth of perpetual luxury growth was beginning to crack. Worse yet, Kering lacked a second-tier brand to absorb the hit. The cracks in the house were no longer cosmetic—they were structural.

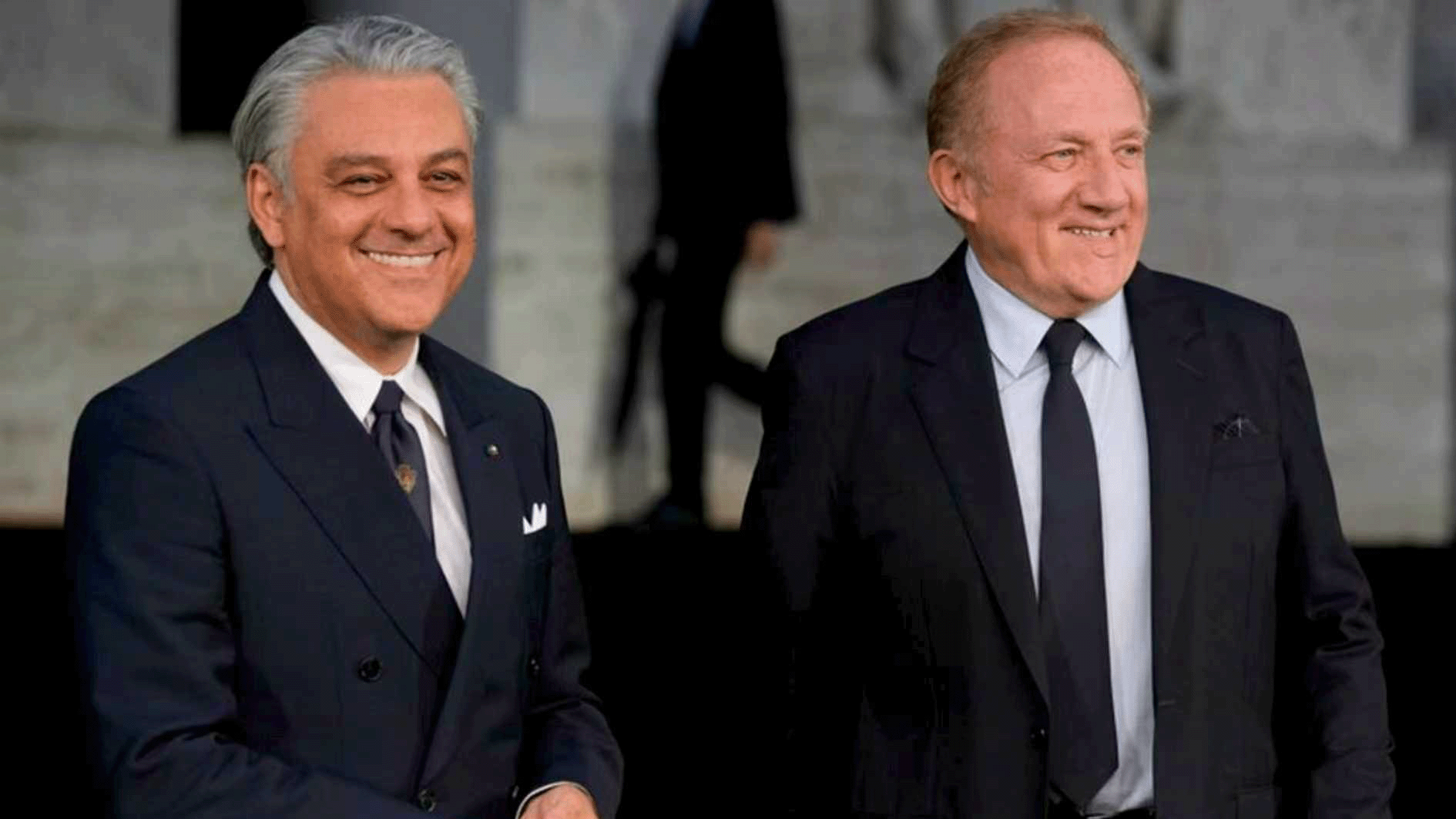

In response, the group launched one of the most ambitious internal overhauls in its history, starting with leadership. In June 2025, Kering announced that François-Henri Pinault would step down from his role as CEO, handing the reins to former Renault Group chief executive Luca de Meo. Pinault would transition to a non-executive chairman role, focusing on long-term strategy. The market responded immediately: Kering shares spiked 12.5% the day the news broke, and doubled in value over the following months.

The message was clear. Kering was no longer operating as a family-run fiefdom, but as a corporation prioritizing operating efficiency, asset discipline, and industrial logic. De Meo’s appointment signaled a pivot from creative romanticism to managerial realism.

Just one month into his tenure, De Meo made a shock move: selling off Kering Beauté—the newly built in-house beauty division launched only two years prior—to L’Oréal for €4 billion. The sale included not just Creed, the niche fragrance brand Kering had acquired for €3.5 billion, but also exclusive licensing rights for Kering’s fashion brands’ beauty lines for the next 50 years. Post-2028, Gucci’s beauty license would also shift from Coty to L’Oréal. A joint venture between the two giants was also announced, laying the groundwork for potential future collaborations in wellness and luxury segments.

For L’Oréal, this was a windfall. It gained Creed, shored up its existing YSL license, and extended its reach into Bottega Veneta and Balenciaga beauty. If the group’s rumored pursuit of Armani beauty also materializes, L’Oréal would command an unrivaled portfolio in high-end fragrance and cosmetics.

For Kering, the move was more sobering. It parted ways with a business that had shown signs of promise—beauty was one of only two growing categories in its most recent H1 2025 earnings, with Creed delivering a 9% year-on-year increase. But De Meo saw something else: a chance to streamline the balance sheet, shed non-core burdens, and reclaim operational agility. Better to lease brand equity to beauty experts and redirect resources to core fashion categories where Kering had both legacy and know-how.

In parallel, the group pressed pause on acquiring Valentino, delaying its call option to fully purchase the brand until 2028. The original agreement would have required a decision as early as 2026, hanging a multi-billion-euro liability over Kering’s balance sheet. Postponing that risk was a form of quiet defense, especially as Gucci’s recovery remained uncertain and free cash flow was under pressure. A €100 million emergency investment was still injected into Valentino’s parent company to stabilize its fragile finances—more a protective moat than an acquisition runway.

Internally, De Meo began reengineering the company from the ground up. He reshuffled Kering’s leadership, bringing in former Renault executives to helm finance and marketing roles at Gucci. These included Gianluca de Ficchy as CFO and Giovanni Perosino as SVP of global marketing, along with Philippine de Schonen to lead investor relations at the group level. The signal: operational rigor would now coexist with creative experimentation.

Consulting giants Bain and BCG were drafted in to run full diagnostic reviews of the group’s brands. Bain took Gucci, while BCG oversaw YSL, Bottega Veneta, and Balenciaga—each tasked with dissecting SKU strategy, pricing, channel effectiveness, and store network efficiency. De Meo’s aim was not to consolidate creative control, but to shift the system towards data-driven accountability, reducing the group’s historic over-reliance on Gucci.

He also pushed for a more consumer-centric approach, shortening product development cycles and decoupling growth from the whims of creative directors. In a departure from luxury norms, De Meo made it clear that Kering’s brands would need to start operating less like ateliers and more like industrially-minded business units.

This pragmatism extended to innovation strategy. In a rare move for a luxury group, Kering launched its own investment vehicle, the House of Dreams division, to scout next-gen opportunities beyond traditional fashion. Its first bet: a joint investment in the Chinese high-end gold jewelry brand Borland Jewel (寶蘭), alongside Challenger Ventures and Shunwei Capital. The move marked Kering’s first foray into early-stage investment in China’s local heritage categories—another sign of De Meo’s willingness to test new growth stories.

Creative leadership also underwent a dramatic shift across Kering’s key houses.

At Gucci, a bold pivot took shape. With Sabato De Sarno’s minimalist reset failing to reignite interest, Kering pulled a surprise move by assigning Demna—Balenciaga’s polarizing star designer—to take over. His debut collection, “Gucci La Famiglia,” staged during the SS26 Milan shows, fused cinematic nostalgia with family theatrics, reviving house codes like the Bamboo and Jackie bags with a maximalist flair. The show succeeded in reigniting social media buzz, and early signs pointed to an uptick in store foot traffic.

Interestingly, Demna’s reworking of 1990s Gucci silhouettes struck a chord with male consumers—an often under-leveraged demographic in luxury. If Demna can sustain this attention, convert it into bestselling bags and shoes, and find a midpoint between “it-brand” hype and investment-grade design, Gucci may be on the cusp of a real turnaround. But the next few seasons will be critical.

Bottega Veneta, in contrast, chose stability. Under new creative director Louise Trotter, the brand leaned into craft, wearability, and tactile depth—moving away from avant-garde silhouettes and conceptual storytelling. The result: steady single-digit growth, with ready-to-wear and footwear as highlights. While not headline-grabbing, BV remains Kering’s cash-flow engine, tasked with underwriting Gucci’s more volatile repositioning.

At Balenciaga, the departure of Demna necessitated a reorientation. Pierpaolo Piccioli, known for his poetic couture at Valentino, was tapped to cleanse and recalibrate the brand’s image. His debut maintained architectural references while softening the tone—though it lacked breakout accessories with commercial bite. The absence of a new “it-bag” or viral footwear moment underscored how hard it would be to replicate Demna’s merchandising magic, even as the house pursued a quieter elegance.

As 2026 approaches, the group faces a series of open questions. Can Gucci maintain momentum without blurring lines with Balenciaga? Will McQueen or Brioni—still struggling for relevance—receive sufficient investment? Can Piccioli’s Balenciaga find its own creative identity without defaulting to Valentino’s playbook? The goal is a balanced portfolio: Gucci for scale and cultural heat, BV and YSL for dependable profitability, Balenciaga and McQueen for edge and image, and Brioni for ultra-high-net-worth men. Any deviation risks destabilizing the entire system.

For now, Kering has shifted from freefall to deceleration. The reforms orchestrated by De Meo—however painful—have bought the group time. In 2026, three indicators will determine whether the gamble is paying off: a reversal of Gucci’s sales contraction, a recovery in group profit margins, and a meaningful reduction in net debt.

Only if all three materialize can Kering confidently return to the negotiation table of valuation peers like LVMH and Hermès.

But there is one area where Kering has arguably outthought—and outpaced—its peers: deep, strategic commitment to the Chinese market. Unlike Louis Vuitton, which deployed a monumental cruise ship-shaped structure in the heart of Shanghai for a short-term spectacle and sales spike, Kering has taken a more long-termist, values-driven approach to embedding itself within China’s cultural fabric.

On one front, it has strengthened its partnership with the Shanghai International Film Festival, leveraging its “Women in Motion” initiative to spotlight and support female filmmakers in China. On another, it has backed local innovation through sustainability awards. Most recently, at the 2025 China International Import Expo, Kering announced its new partnership with Shanghai Fashion Week: the “Kering CRAFT Creative Residency Program,” aimed at building exchange and co-creation channels for Chinese designers between Shanghai, Milan, and Paris.

These efforts are unlikely to yield immediate commercial returns. But they serve a different, equally strategic purpose: Kering is branding itself not merely as a luxury conglomerate selling bags and shoes, but as a cultural stakeholder and value-driven corporate citizen in China. It’s less concerned with social media virality, and more focused on cultivating a new generation of creative talent, institutions, and cultural capital.

Zooming out, when these actions are viewed alongside the establishment of Kering’s “House of Dreams” investment division and recent venture investments, a longer-term narrative begins to emerge: Kering is betting not just on luxury consumption in China, but on the rise of local Chinese brands. It’s using capital, networks, and infrastructure to place itself inside China’s next wave of brand building.

Nowhere is this more evident than in its recent investment in Borland Jewel, a high-end Chinese gold jewelry label founded just four years ago. Despite operating only three physical boutiques, Baolan has gained a cult following among Chinese Gen-Z consumers thanks to its revival of ancient goldsmithing and filigree techniques.

Kering’s entry into Borland Jewel came through its venture arm, established in 2019. The logic is twofold. Financially, the timing is savvy: Chinese gold consumption is surging, and high-end gold products now combine emotional symbolism with financial attributes—creating a compelling hybrid asset class. Strategically, Kering recognizes a structural shift in the market. While China may not soon produce a global-scale luxury brand in leather goods or ready-to-wear, the jewelry sector—with its deep cultural roots and perceived asset value—presents real potential for a Chinese brand to scale globally.

For Kering, backing Borland Jewel isn’t just about a short-term equity gain. It’s a calculated early-stage bet on the next Chinese narrative.

Taken together, these moves reveal a group at a crossroads, but also one willing to confront its own structural flaws. In 2025, Kering acknowledged that its old playbook no longer worked. It invited discomfort, financial pruning, and creative upheaval. Bringing in a crisis-hardened CEO like Luca de Meo is, at its core, a wager: can someone from outside the fashion elite infuse industrial logic, financial discipline, and systems thinking into an industry governed by emotion and symbols?

If the bet pays off, Kering’s transformation—from contraction to recalibration—could become a textbook case of corporate reinvention during a downcycle. But failure is not an option. For De Meo and Kering, there is no Plan B. 2025 was about diagnosing the problem and reshuffling the deck. From 2026 onwards, every quarterly earnings report and fashion show must serve as proof that this transformation is not just performative self-rescue, but a decisive rewriting of the group’s future.